The venue had changed to Frankfurt, but this year’s Digital Signage Summit Europe provided a just as wide range of viewpoints about digital signage (DS) and digital out of home (DOOH) as ever. Here are six key points that we took away from the event.

1. The market is changing in various ways

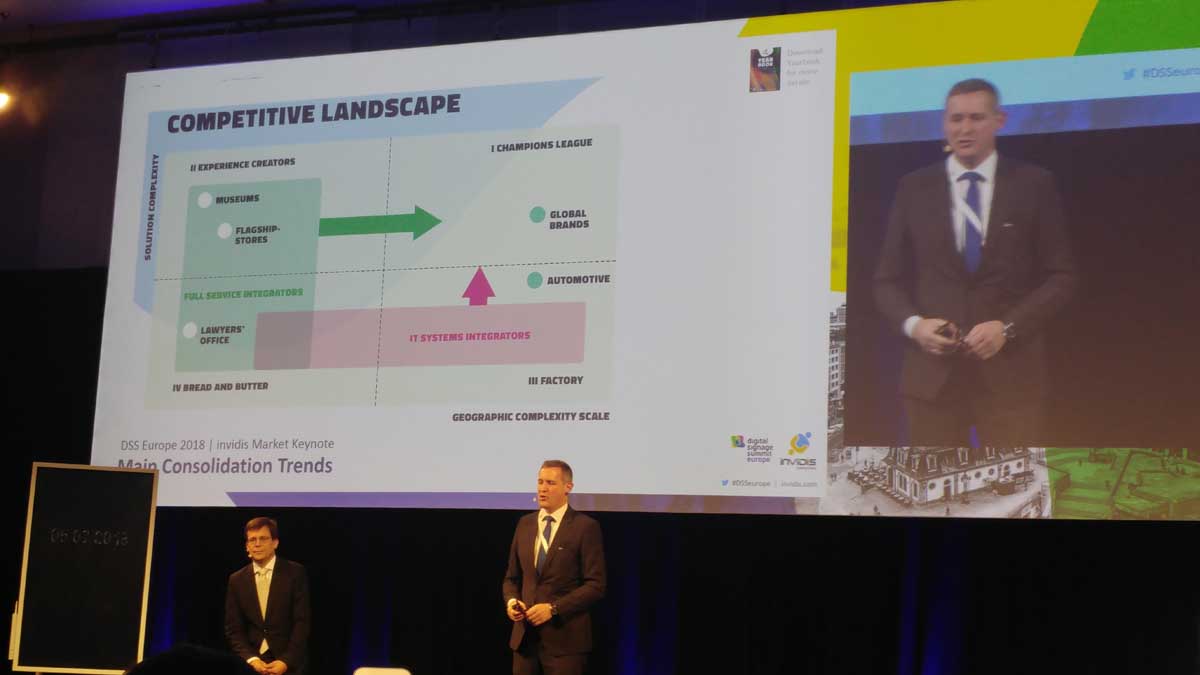

Last year saw more than 100 mergers or acquisitions, noted conference chair Florian Rotberg, though nothing had the impact of Stratacache’s acquisition of Scala the year before.

As the market matures, full-service integrators are acquiring companies to increase the geographic complexity of their offering, while IT system integrators (who are “fantastic at industrialising any kind of service”) are buying expertise to increase their solution complexity.

However, he warned that “it’s the end of the ideal world for most full-service integrators” who “make money… from deployment and operations and also concept”. They face a choice: “Either you grow big – and that means really big – or you need to specialise.” Additionally, a weakness of many integrators is their inability to “industrialise”. In the past, every small project was different, but for multinational rollouts of thousands of screens, “Everything needs to be professional, every process needs to be defined – industrialisation is so essential.”

2. New types of companies are becoming involved

Rotberg noted that “a lot of global players are entering the market through the back door”. Taking the German car market as an example, he noted that the main brands’ signage contracts are all with general contractors with no specific DS experience. These are professional service firms such as Accenture, PwC and Deloitte – who then subcontract to signage integrators.

Another significant new player – which “two years ago no-one would have thought of” – is an IT finance company called Econocom, which has acquired three leading digital signage companies in Spain since February 2017. “They can add something that most system integrators cannot add right now – they are big, they have finance power, and they can change the screens more often.” The company does this by providing new displays to its biggest customers after a couple of years (rather than five or so) and remarketing the old ones elsewhere.

Subsidiaries or special agencies of global advertising and marketing groups (such as WPP, Omnicom and IPG) are likely to be the next market consolidator. Currently these companies are subcontracting their DS requiremetns to specialists, but soon will be taking a “make or buy” decision, said Rotberg.

3. The importance of data

“The industry has changed from Mad Men to Math Men… everything is driven by data,” said Rotberg in the opening keynote. “If you don’t know how to connect your digital touch points with ERP, with everything in the back office, you’re lost.”

With the increasing use of sensors, the role of data in DOOH is only going to grow. Chairing a panel on sensors and AI, Stefan Schiecker of ResultMC identified three uses for data from sensors: analysing historical data, using live data for real-time triggering, and making predictions from data, such as determining when queues are likely to build.

Panel member Andreas Biss of NEC commented that, when designing systems to play content based on the demographic make-up of people passing by, age and gender detection are not enough. “Solving the problem of who will be relevant in two seconds’ time, when the current video stops playing” requires more technologies, to understand walking patterns, for example. “Trying to understand people’s behaviour is very complex.”

Talking about DOOH in a multiscreen strategy, Hoss Khoravi of Visual Art sounded a note of caution about data. He said that he felt that a view expounded at a seminar he attended a couple of years ago, that out-of-home was useless without data about the person in front of the screen at that moment, went too far – it wasn’t an evolution of DOOH, it was turning it into something very different – he drew a parallel with Robocop.

He feels that his company, which is the only vendor in the Nordics that offers programmatic, has “a foot in the old way and the new way”. One example was a campaign for mobile provider Halebop, which sought to turn train delays into a positive thing by giving passengers extra free mobile data. This was done by running advertisements with a download code at relevant stations when delays had occurred.

4. More individualised, but not personal

Real-time programmatic advertising can create a more individualised experience. Among the examples given by Richard Offermann – managing director, Ströer Digital Group – in his presentation on the customer journey, was an ebay campaign in shopping malls and railway stations that created time-limited offers based on current stock availability and the promotional activity of competitors.

However, this is still a one-to-many medium: “Really individualising it – recognising who is in front of the screen and then displaying a product for this individual person – might not be possible in a public area.” But it makes sense to think of target groups: as he pointed out, the people in the main Frankfurt station at 7:00 on a Monday morning and on a Saturday afternoon are two very different audiences.

So while knowing more about the audience is important, reach is still an important metric, said Peer Schmitz-Kuo of Media Frankfurt and Andreas Prasse of Wall (part of JCDecaux). With the proportion of the world’s population based in cities set to rise to 80% by 2050, and air traffic set to double in the next 25 years, the reach of displays in major city locations and airports will keep an upward trajectory.

5. The speed of change is increasing

Both customer attitudes and the capabilities of technology are changing more quickly than ever.

In his keynote on ‘retail design meets digital’, Alastair Kean of retail experience agency Dalziel and Pow commented that “customers have changed more in the last five years than in the last 25. They’re more switched on, less loyal, more empowered, having the whole world at their fingertips… People are more immune [to advertising] and more sceptical, customers do the talking and the brands have to increasingly listen, and also be transparent and shareable.”

The speed of technological progress was discussed by Offermann. “The worst thing you can do predicting the future is taking the speed of growth at the moment and extrapolating it,” he said.

He believes that as human beings, we find it difficult to “think exponentially into the future”. This leads to what he calls the “exponential growth surprise factor” – the gap between steady progress and a quantum. One example he gave was the way that mobile phones developed in recent years, adding cloud communication and heavy internet use to what was previously a fairly simple voice device.

6. Consider the physical space

We shouldn’t forget that digital experiences take place in a physical environment, and the former should not obliterate the latter.

This point came out in two very different presentations. In a wide-ranging keynote about ‘rebooting your personal future’, Raphael Gielgen, a futurist working for furniture company Vitra, cited an article by journalist Jen Murphy. After a stay in a very ordinary hotel, where most interactions were with screens rather than people, she came to the conclusion that airbnb is so successful because it has the personal touch that is missing from much high-tech hospitality.

“airbnb locates people,” said Gielgen. People want to be located – nobody wants a generic space experience. Creative people need to understand what is the duty of a space… I would say the duty of a physical space is to bring people together to have real human connections.”

Michael Luck Schneider of ESI Design presented some of his company’s large-scale media canvas projects that have “transformed buildings into experiences”, and talked about the very detailed processes by which this content is created and matched to the space.

He said that most media displays in physical spaces presents the viewer with a choice between “entering the world that lives on the other side that window – in which case why are you in that physical space anyway?” or ignoring it. Instead, ESI’s media displays, many of which are in corporate lobbies, are designed to support the space – enhancing the architecture, capable of being viewed from various distances, with content that matches the “speed” of the space.

Although these displays can cover a large area, it’s important not to be too dominant. He gave the example of a Denver installation with five LED columns that are 90ft high, but only about the width of a person across. From a distance they look like five slices of a single view, but close-up, each column is human-scale. “This could have been done as a single LED display,” he said, “but I don’t think it would feel very good to be a human being in this space, because the scale of it compared to you would have been overpowering.”